Key Takeaways

Both finance and lease let you drive a car without paying the full price upfront.

Monthly payments differ because you pay for ownership with finance and depreciation with lease.

Your driving habits, budget, and long-term plans determine which option suits you better.

Each choice has trade-offs between lower payments now and ownership benefits later.

Overview: Difference Between Finance and Lease

Finance and lease are two ways to get a car without paying everything upfront. They seem similar, but they work very differently.

What is Financing?

When you finance a car, you’re buying it. A bank or lender gives you money to pay for the vehicle.

You make monthly payments over time, usually three to seven years. Each payment includes the loan amount plus interest.

Once you finish paying, the car is yours. You own it completely and can keep it as long as you want.

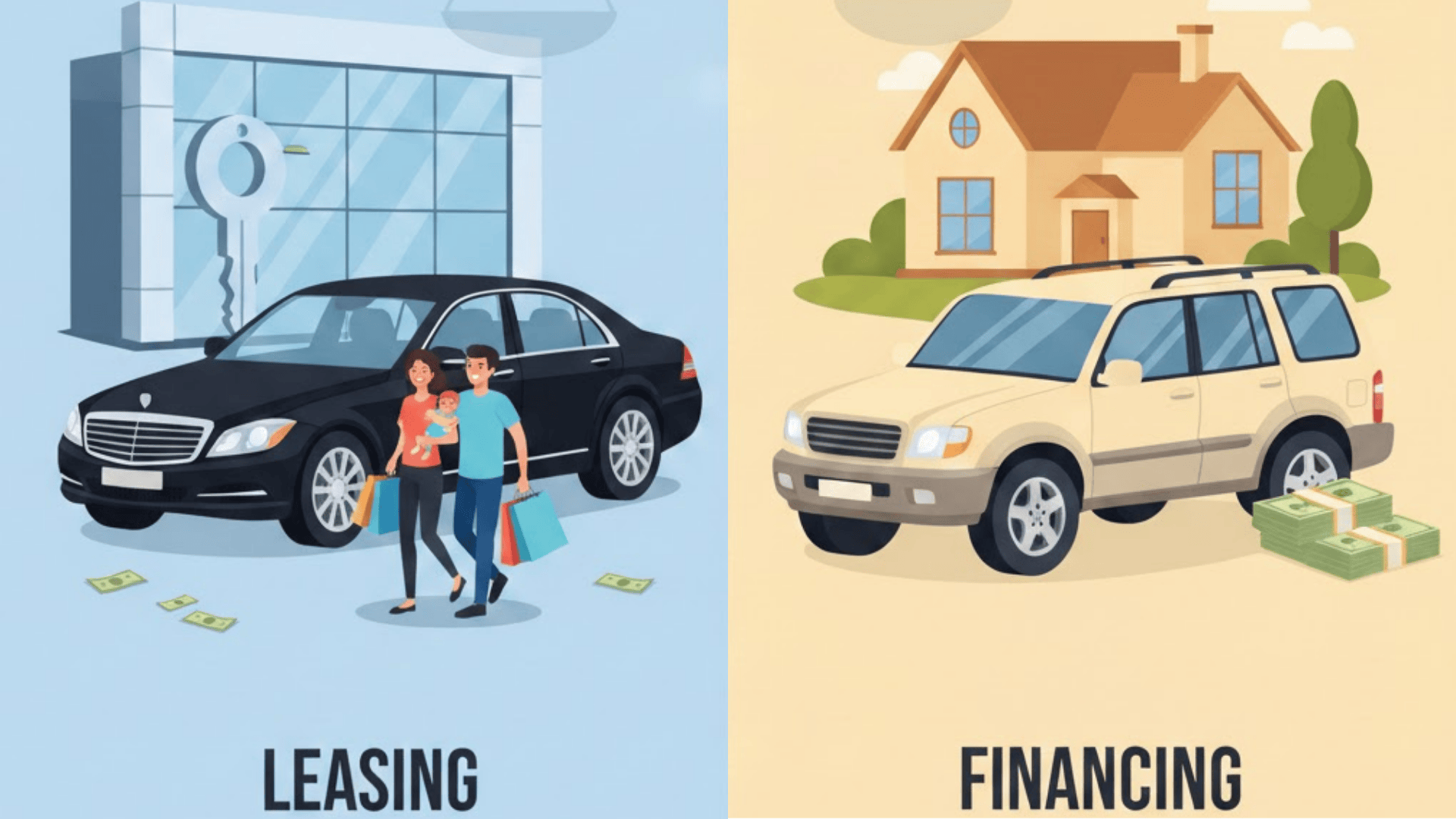

What is Leasing?

Leasing is more like renting a car for a set period. You pay monthly for the right to use the vehicle, typically for two to four years. The lease company owns the car, not you.

Your payments cover the depreciation during your lease. Mileage limits are usually 10,000 to 15,000 miles annually.

Return the car in good condition with normal wear, at least end, you may return it or buy it.

Key Difference Between Finance and Lease

Here’s what sets these two options apart. Knowing these differences helps you pick the right choice for your needs.

Ownership

When you finance, you own the car from day one. The lender has a lien until you pay off the loan.

After that, it’s completely yours. With leasing, you never own the vehicle. The leasing company keeps ownership the entire time. You’re just using their car for a fixed period.

Monthly Payment Amount

Lease payments are usually lower because you’re only paying for the car’s depreciation. You’re not covering the full vehicle cost. Finance payments tend to be higher since you’re buying the entire car.

Your monthly bill includes both the principal amount and interest charges on your loan.

Total Cost Over Time

Financing costs more upfront but saves money long-term.

You pay interest, but once the loan ends, you have no more payments.

Leasing seems cheaper monthly, yet you keep paying forever if you always lease. You never stop making payments because you never own anything.

Flexibility and Commitment

Ending a lease early comes with steep penalties and fees. You’re locked into your contract terms.

Financing gives you more freedom. You can sell or trade your car anytime, though you must pay off the remaining loan balance first.

What’s the Difference Between Lease and Finance for Buyers?

Different buyers have different needs. Here’s what helps you decide which option works best for each situation.

Best Option for Daily Long-Term Drivers: Finance is your best bet if you drive a lot and plan to keep your car for years. You won’t worry about mileage limits. The car becomes yours after payments end.

Best Option for Short-Term Use: Leasing works better when you want a new car every few years. You get the latest models and features regularly. Just return the car and lease another one when your term ends.

Best Option for Budget-Focused Buyers: Finance wins if you want to save money over time. Your payments stop eventually, and you own an asset. You can drive it for years without any more monthly bills.

Best Option for Business Use: Leasing offers tax benefits for businesses since payments are deductible expenses. You can write off the cost each month. Plus, you always have reliable, newer vehicles for your company’s needs.

Lease vs Finance: Payment Structure Explained

| Aspect | Finance | Lease |

|---|---|---|

| What You Pay For | Full car price plus interest | Depreciation during the lease term |

| Down Payment | Usually, 10-20% of the price | Lower, often 0-10% |

| Monthly Cost | Higher payments | Lower payments |

| Payment Duration | 3-7 years typical | 2-4 years typical |

| After Final Payment | You own the car | Return or buy the car |

| Mileage Charges | None | Fees for exceeding the limit |

| Wear and Tear | Your responsibility | Charged at lease end |

| Early Termination | Pay off the remaining balance | Heavy penalties apply |

Pros and Cons of Leasing and Financing

Every option has its ups and downs. Let’s walk through what works and what doesn’t for each choice.

Pros of Financing

- You Build Equity Over Time: Each payment increases your ownership, making the car a tradable asset later.

- No Mileage Restrictions: There are no penalties for putting extra miles on your vehicle.

- Complete Freedom After Payoff: Once you finish payments, the car is yours. No more monthly bills.

- Customize as You Wish: Modify or personalize your car however you like. It’s yours to change and upgrade.

Cons of Financing

- Higher Monthly Payments: Your bills are larger since you’re paying for the entire vehicle. This pulls your budget.

- Depreciation Hits You: The car loses value over time. You might owe more than it’s worth initially.

- Maintenance Costs Add Up: After the warranty expires, all repairs come out of your pocket.

- Stuck with One Car Longer: You can’t easily switch to a newer model. You’re committed until the loan is paid off.

Pros of Leasing

- Lower Monthly Payments: You pay less each month. This frees up cash for other expenses.

- Drive Newer Cars Often: Get a new vehicle every few years. You have the latest features and technology.

- Warranty Usually Covers Repairs: Most leases fall within the manufacturer’s warranty period.

- Lower Sales Tax: You only pay tax on the lease payments. This saves money compared to the full price.

Cons of Leasing

- Never Own the Vehicle: You’re making payments but never building equity. The car never becomes yours.

- Mileage Limits Apply: Exceed your allowed miles, and you pay extra fees. These charges add up quickly.

- Wear and Tear Charges: Return the car with damage, and you’ll pay penalties. Even normal wear can cost a lot.

- Early Exit Is Expensive: Breaking a lease costs thousands in penalties. You’re locked into the full term

What Factors Should You Consider when Leasing or Financing

Choosing between lease and finance isn’t simple. You need to think about several factors to make your decision.

Your Driving Habits and Mileage Needs

If you have a long commute or take frequent road trips, financing makes more sense. Leasing restricts your mileage, and going over costs extra. High-mileage drivers should finance to avoid penalties.

Your Budget and Monthly Cash Flow

Look at what you can afford each month. Leasing offers lower payments, which helps if cash is tight right now.

Financing costs more monthly but saves money long-term. Consider your income stability and other expenses before deciding.

How Long You Plan to Keep the Car

Do you want a new car every few years or keep one for a decade? Leasing suits people who like upgrading often.

Financing works better if you plan to drive the car for many years after payments end.

Your Credit Score and Interest Rates

Better credit gets you lower interest rates on both options.

Poor credit might limit your choices or increase costs. Check your credit score first and see what rates lenders offer you before choosing.

Tax Benefits and Business Use

Businesses can deduct lease payments as expenses, which reduces taxable income. Personal buyers don’t get the same tax advantages, so this matters mainly for company vehicles.

Maintenance and Repair Costs

Think about upkeep expenses over time. Leased cars usually stay under warranty, so repairs cost less.

Financed cars require more maintenance, with costs falling on you. Budget for these future expenses.

What People Say About Lease vs Finance

Most people agree that the biggest difference between leasing and financing is ownership.

With financing, you own the car and can sell it later, even after it loses value. Many say depreciation is not a real problem because cars rarely drop to zero value and still serve daily needs.

Leasing supporters point out lower monthly payments and the chance to drive a new car every few years.

Critics say leasing still makes you pay for depreciation, plus mileage limits and extra fees can add up.

Several users stress that leasing only makes sense with strong deals and honest mileage estimates.

Overall, people suggest running the numbers and choosing what fits your driving habits and budget.

Final Thoughts

Which option is right for you? It depends on your situation. Just remember the mileage limits and return conditions.

Think about your budget, driving habits, and long-term goals. Do the math on total costs over several years.

Check what you can afford each month, and don’t rush your decision.

Both options have their place. Neither is wrong nor right for everyone. Pick the one that fits your lifestyle and financial situation best. Your needs matter most here.

Need help deciding? Talk to a financial advisor or dealer about your specific circumstances.